Also assume that actual costs for purchasing and receiving are $60,000 fixed costs and $39,000 variable costs. Both departments should be allocated ignoring the reciprocal services.d. The net realizable value method and NRV less an average profit margin method are not needed in this case because the products have identifiable market values at the split-offpoint. The self services (the 50 KWH’s used by S1 and the 30 labor hours used by S2) are ignored along with the reciprocal services (the 100 KWH’s used by S2and the 20 labor hours used by S1) in developing the proportions.

Module 7: Costing Methods

It accurately accounts for the mutual services provided among service departments. The step-down method is useful in situations where there are multiple service departments and some serve others more than they are served. It allows for a more distinct tracing of costs, improving the accuracy of indirect cost allocation. However, it can be somewhat arbitrary in terms of deciding which department’s costs should be allocated first.

Accounting for Managers

Can joint costs be allocated to joint products based on a “cause and effect” relationship? Custodial services on the other hand, may be better allocated based on the square footage of each of the operating departments. If the press area (process 1) of the Ultimate Planner business occupies 10,000 square feet, while the packaging area only occupies 2,000 square feet, it probably takes more custodial effort in the press area! In this method, we will be ignoring the fact that one service department may offer services to another service department. For example, the HR department will offer services to the accounting department by hiring staff and providing training.

- Theserelationships affect the choice of allocation methods, as well as the accuracy of the first stage cost allocations.

- Therefore, it is essential that decision-makers view cost allocation as not just a financial concern but a critical aspect of their CSR and sustainability efforts.

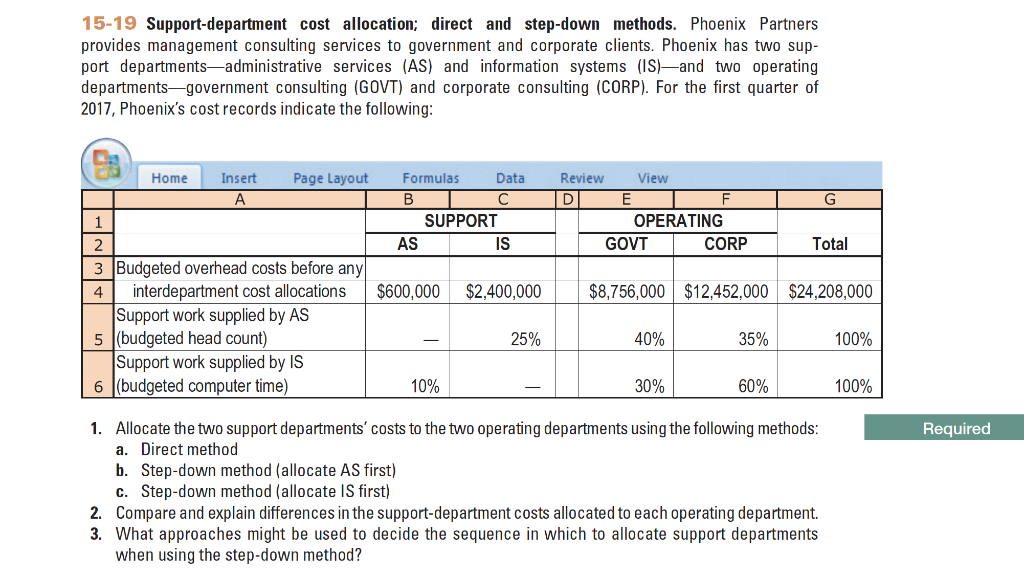

- The Cutright Company has a small factory with two service departments and two producing departments.

- Costs are not allocated back to a department that has already had all of its costs allocated.

Step Four: Allocate Variable Costs Among Departments or Projects

For example, for performance evaluation and motivation purposes, the “fairness and equity” logic is sometimes moreappropriate for common administrative and facility related costs. Examples include top management salaries, internal auditing, company legal and medicalfacilities, advertising designed to promote the company image, public relations and landscaping around the facility. From the “fairness and equity”perspective, one could argue that these costs should not be allocated at all, or if they are allocated to the various what is modified adjusted gross income magi segments of a company, the “ability tobear” logic should be used. In contrast to direct allocation, the step-down method, also known as the sequential method or the stair-step method, allows for a more comprehensive spread of costs. This method begins with allocating the costs of the service department that provides the most services to other service departments. The total cost of each service department, including the allocated costs, is allocated step-by-step until all service departments have been allocated.

Common Mistakes People Make When Allocating Costs

Service cost centres are those that exist to provide services to other cost centres in the organisation. Consequently, their costs must be re-apportioned to production cost centres so that their overheads can be absorbed into the final product. This article looks at the various methods of re-apportioning service cost centre costs.

There’s also a simple way called the direct materials cost method that uses an allocation base of the same value as the variable rate. Using FAC or Variable costing can provide more accurate reporting on your company’s financials. Discuss how a plant wide overhead rate tends to distort product costs.

In that case, you will need to construct a cost-allocation plan that reflects the allocation of overhead expenses between these areas. Taking these factors into account when allocating cost allows businesses and individuals to understand better how much money they need coming in (revenue) compared with how much they must spend (costs). Below shows how the variable costs change as the number of chairs made varies. Determine the difference in the total operating cost if electricity were purchased externally and indicate whether the company should make or buy electricity.

If Product Xconsumes 20 percent of one indirect resource within a department, it must consume 20 percent of all of the indirect resources within the department andthe allocation basis must reflect this percentage. Otherwise a single departmental rate will not provide accurate product costs. Discuss the different conceptual bases for allocating costs to cost objects.3.

How a company chooses to allocate its costs is a reflection of its values and priorities. If sustainability and ethics are prioritized, cost allocation will support corresponding initiatives. If not, cost allocation can inadvertently communicate non-commitment to external stakeholders, potentially adversely affecting the organization’s reputation and market position. In summary, the process of cost allocation serves to bridge the gap between operational activities and financial management. This linkage is vital in making strategic business decisions, from setting product prices to planning budgets to making investment decisions. Therefore, understanding cost allocation is fundamental to business’ financial success.

Certainly, approximations of the true costs are better than these confusing cross-subsidies. The plant wide rates provide inaccurate product costs because the products do not consume the indirect resources in the same proportions in each of the two departments. The step-down, or sequential method, ignores self services, but allows for a partial recognition of reciprocal services. As a result, the step-down method is different from thedirect method in that some service department costs are allocated to other service departments. Equations forthe service departments [1] are developed to allocate the service department costs in sequence starting with the department that serves the greatest numberof other service departments.